$TARO Deep Dive (PT: $81)

$TARO Deep Dive (PT: $81)

The quiet buyout situation that they (seriously) don't want you to know about. BYOA (bring your own activist!)

Hi all - your weekend read is below! Feel free to reach out with questions or for more info.

DISCLAIMER: This report is based on my personal opinion and experience and should not be considered professional investment advice. This idea or strategy should never be used without assessing your own personal and financial situation, or without consulting a financial professional. This trade especially is unsuitable for most investors. I may or may not have a position in TARO and reserve the right to enter/exit positions without updating this report or notifying subscribers. Please see the bottom for a full disclaimer.

Core Business

Taro was established in Israel in 1950, and first went public on OTC markets through an IPO in 1961. Initially producing pharmaceutical ingredients, Taro shifted gears following the Hatch-Waxman Act (aka as the Drug Price Competition and Patent Term Restoration Act) in 1984, which set up the North American generics market. Taro’s 1984 acquisition of K-Line Pharmaceuticals, a generic dermatological medication company, would define the company’s niche for the next few decades.

Enter Sun Pharmaceuticals: A Motivated Acquirer

In 2007, Taro was in dire straits, facing bond payments with no capital or available credit. Sun Pharmaceuticals’ majority owner and Chairman Dilip Shanghvi negotiated with Taro founding owner and Chairman Barrie Levitt to structure a merger and a $60mm cash influx to save Taro – in the event the merger wasn’t consummated pursuant to a shareholder vote, Sun was granted the option to purchase the ordinary and founding shares of Taro Directors and initiate a Special Tender Offer for remaining Taro shares at $7.75. In 2008, with the merger unconsummated, the legal fight began, as Chairman Levitt sought to retain control of his company and Shanghvi alleged fraud and misrepresentation.

In 2010, Taro’s complaint was dismissed, and Sun Pharmaceuticals took possession of all Taro founders shares, entitled to 1/3 of Taro voting power, and 66.3% of outstanding ordinary shares for $273mm. Sun had expressed interest in a complete buyout in 2007 (the option at $7.75) – Shanghvi evidently remembered, and followed up with buyout offers for Taro shareholders at patently insulting prices:

2011: $24.50 @ 7.2x EBITDA

2012: $39.50 @ 4.8x EBITDA

Taro minority shareholders held firm and rejected the offers. Grand Slam Asset Management, in a public letter to Sun, noted the multiple decrease between the two offers and argued for a 15x LTM EBITDA multiple on the business, with a $100+ fair takeout price. Taro’s generics strength from 2010-2013 preceded a meteoric rise in Taro’s share price.

Sun saw the writing on the wall and terminated the tender offer; at this point, Sun and Dilip Shanghvi already had 66.30% beneficial ownership of Taro Pharmaceuticals, and 77.3% of voting power. Instead, Sun decided on an alternative plan. With the founders shares and control of Taro’s FCF machine, Sun could control Taro to buy back shares on the open market, slowly but surely increasing the ownership share of Sun.

For the past decade, that’s exactly the strategy Sun has followed – Taro has spent over $750mm of its cash on buybacks since 2014, increasing Sun’s ownership from 66% to 78% without Sun spending a penny. The table below illustrates ownership and repurchases. Note the repurchase prices – well over double the current stock price just last year.

Considering Taro’s one-time special dividend of $500mm in FY2019, when Sun had approximately 75% beneficial ownership, Sun has already made $375mm on its $273mm initial outlay, pre-tax.

Sun Pharmaceuticals is an experienced acquirer – three pages of their annual report are dedicated to listing investments in associates, subsidiaries, and other controlled business. What makes Taro unique is its importance to the parent company, while still remaining just a footnote in Sun’s statements and reports. Even with all the public filings of Taro easily accessible, equity research analysts of Sun Pharmaceuticals can provide no more than a cursory overview of the business.

The Edge: How did the market miss this?

Taro is an under-the-radar name that screens abysmally. Most buy-side screeners would eliminate it for the lack of float alone (discussed in Trade Feasibility), and the rest would struggle to get past the following points:

Declining margins from dermatological generics pricing pressures.

Significant EBITDA adjustments in the past two years, not accounted for by data sources like FactSet or Bloomberg.

No analyst coverage or recent earnings calls.

Until recent years, unresolved litigation risk.

The above risks are further discussed in the Risks section of this report.

Management itself is remarkably inaccessible. The investor relations number on the website leads to an old line with a defunct answering machine; wait all you want, it won’t work. I’ve never received a response from the IR email either. The number from recent filings works; through undue persistence over the past four months, I’ve spoken with the CFO’s assistant twice, who was remarkably unhelpful in scheduling a call.

I would speculate that obstructing investors from realizing Sun’s strategy, or from treating the business as properly investable, drives Taro’s stock price down to levels where Sun could acquire the business for pennies on the dollar, even with a substantial premium to minority shareholders.

Thesis 1: Dermatological Performance Stabilizing

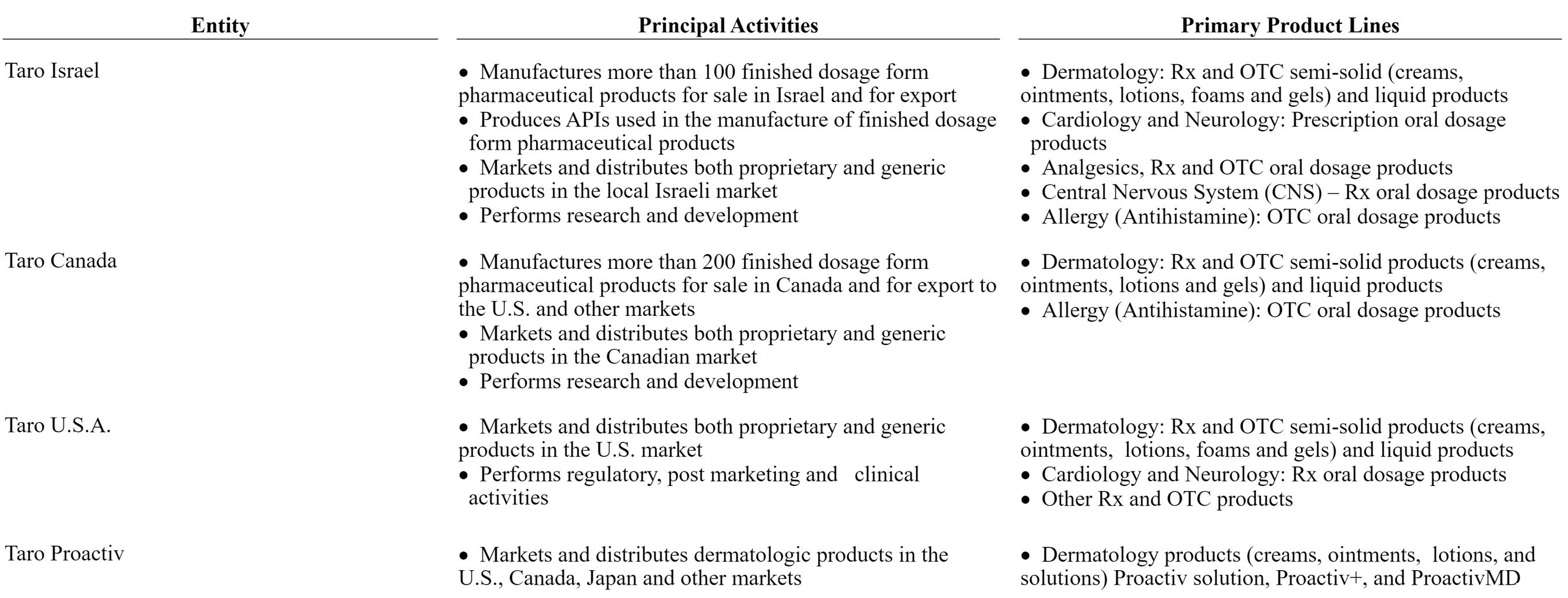

Dermatological medicine is naturally reoccurring business. It’s difficult, nearly impossible, to ‘cure’ the root cause of acne, psoriasis, or other skin conditions. Instead, you treat the symptoms using dermatology products offered in no small part by Taro Pharmaceuticals. The snip below describes Taro’s lines of business.

In 2022, Taro’s largest markets were the U.S. (67% of sales) and Canada (23% of sales). Taro’s sales are primarily through drug wholesalers and store chains, alongside merchandisers and other distributors who sell to consumers.

Margins are an important point to address here. Taro has faced declining gross margins since 2016, driven by a fall across the board in dermatological generics pricing, as well as a concurrent rise in input prices.

On the 3Q2023 earnings press release, Taro’s CEO Uday Baldota stated,

“While we maintain the leading market position of many of our products, we continue to face an overall market trend, particularly in the U.S, that is not dramatically changing, and depending on the product, price deflation continues to be a challenge. With input costs rising sharply, we will continue to allocate increasing amounts of capital including R&D efforts into growth and profitable businesses and new businesses opportunities”.

If you look back to when Baldota first took the role of CEO in 2017, his quote in the 2Q earnings press release then is very similar to his line above on R&D and business development. Every quarter since taking the role, CEO Baldota has delivered a dour market outlook (justifiable, considering the industry trends), a platitude on increasing in R&D, and a continuing evaluation of business development opportunities.

Studying Taro’s statements, the CEO’s comments don’t ring true. R&D expense has been down consistently, dropping 23% from 2016 to 2022. That’s not a hallmark of a business making waves to recapture growth, and the revenues over the same period agree, declining 41% over the same period (however, this comparison doesn’t account for concurrent price deflation that drove revenue down as well).

Over the five years since Baldota took over, Taro has made just one actual investment in business development. In February 2022, Taro acquired Alchemee (the Proactiv Company), “America’s #1 acne routine”, for $90mm. Proactiv is a brand that grew to fame in the age of infomercials with A-list ambassadors (from Justin Bieber in 2010 to Kendall Jenner in 2019), and it’s still getting rave reviews on its distribution channels (DTC, Ulta Beauty Target, etc.). The business is accretive to revenues and adds a strong marketing arm to a generics business with little differentiation. Alchemee’s brand recognition can help fight price deflation for Taro, helping it reposition away from commoditized generics.

As mentioned, Taro has faced margin declines over the past few years, fighting rising input costs and falling prices due to the competitive generics market. One major driver of margin declines was $600mm+ of litigation and settlement expenses, the majority of which were paid and are now in the rearview. The rest have been provisioned for under a settlements and loss contingencies BS line item since 2021.

Vizient’s Summer 2022 Pharmaceutical Market Outlook projects a strong showing for dermatology medicine over the next decade, as the incidence rate of psoriasis, atopic dermatitis, and other skin conditions remain elevated. Taro has a strong set of ANDA Approvals (below, presented on a cumulative basis), and though subject to the same pricing pressures as the rest of the generics industry, has a diversified generics portfolio and can maintain its competitive position if additional capital spend is needed.

The Biden administration has also consistently expressed an interest in promoting competition throughout the prescription drug industry by offering more generic incentives and easing the approval and development process of biosimilar generic products. As initiatives are (and were, in the Inflation Reduction Act) taken to ease the entry of generics manufacturers into new markets and improving the resiliency of supply chains by incentivizing input competition (cheaper costs for Taro), the generics industry should, at minimum, not face significant declines. A few illustrative snips below:

As discussed in valuation, I model a bear case – flat sales, falling marginal investment, a business in decline that still manages to generate high free cash flow. My projections are nowhere near the generics market estimates above; in a business as tough to predict as this one, I’m content with my margin of safety.

Thesis 2: Strong Cash Position

It’s common to see healthcare businesses trading below cash – especially biotech, a business where cash is meant to be spent in R&D. It’s rare to see a company like Taro, with a history of returning capital to shareholders, trading below cash. Admittedly, the return of capital here is targeted to disproportionately benefit the controlling shareholder, Sun Pharma. The cash position is enough to finance 20+ years of R&D at current expenditures – well above the justifiable needs of the business.

In a liquidation scenario, investors can recognize a nearly 10% gain on investment. It’s important also to recognize the business you’re buying in addition to this cash. The Alchemee (Proactiv) acquisition for $90mm earlier this year, and the core generics business that drives cash flows, are both completely free to the investor at Taro’s present valuation.

With Sun’s control of Taro, I believe it’s nearly impossible that the cash assets are frivolously spent. As I’ll discuss in the next thesis, Taro’s net cash position represents 25% of Sun’s consolidated net assets, and no small part of Sun’s profits. That’s not something Sun can ignore or is willing to spend chasing poor investment opportunities. As seen historically, Sun would rather issue a special dividend to itself (and all other minority investors, of course), but would preferably follow the strategy outlined below.

Thesis 3: Sun’s Acquisition Strategy Succeeds

At the current rate of buybacks, Sun will be at 90% of Taro voting power in 2028. Under Israeli law, at 90% of voting rights Sun must make a tender offer to the remaining shares outstanding and be approved by a majority of minority investors if it intends to proceed.

Sun’s strategy around buybacks and its acquisition goal is well-defined. From Taro’s 20-F:

“A tender offer for all of a company’s issued and outstanding shares can only be completed if the acquirer receives sufficient responses such that the acquirer will hold at least 95% of the issued share capital upon consummation of the shareholders’ tenders. Completion of the tender offer also requires approval of a majority of shareholders who do not have a personal interest in the tender offer, unless, following consummation of the tender offer, the acquirer would hold at least 98% of the company’s outstanding shares.”

Israel corporate law has stringent protections for minority investors – and a 2% voting right stake (equivalent to a 3% common stock stake) is enough to force a majority-of-the-minority approval. Under Section 191 of Israeli Companies Law, in such a case courts can direct Sun to buy out Taro shareholders or give instructions to provide a fair buyout price. At minimum, a buyout offer is a premium to cash assets, but that’s not an acceptable offer under any lens, as it discounts all other assets of the business, intellectual and physical.

Despite their size difference, Taro isn’t a business that Sun can let go of easily. First, there are a number of related party transactions between the two companies; the companies have a symbiotic relationship. Taro’s North American footprint is the exclusive distributor for Sun products, receiving a sales and distribution fee from Sun. Sun’s North America operational and management back end is consolidated with Taro under a Services agreement allowing certain employees to work at both companies.

Second, as shown below from Sun Pharmaceutical’s 2022 annual filing, Taro is ~12% of Sun’s consolidated profit or loss. More importantly, it’s 25% of Sun’s consolidated net assets, primarily from its massive cash position.

Divesting Taro is clearly out of the question – rather, Sun is heavily incentivized to increase its ownership as much as possible so that it won’t have to split profits with minority shareholders. Sun’s own financial multiples are improved through this relationship with Taro - losing the business or the cash hurts Sun’s perception in its home market. Instead of trying to cash out through dividends and facing additional taxes, Sun would find it much more efficient to simply complete the acquisition it has wanted for over a decade. From the 79 subsidiaries described in Sun’s annual report, none pay dividends and most are now wholly owned by Sun.

Valuation and Price Target

Valuation is a core piece of this investment. The first component is the discussion around cash – equity is already below the value of marketable securities, accounted for in the cap structure.

Assumptions:

Revenues are adjusted upwards to account for the Alchemee acquisition, and then are flatlined at 0% growth.

Cost of Goods sold, considering trends, is flatlined at 48% of revenues – still up from 18% of revenues in 2016.

Surge in SG&A to account for added Alchemee acquisition costs, which normalizes over time.

R&D follows historical trends.

10% WACC, though Taro won’t need incremental financing.

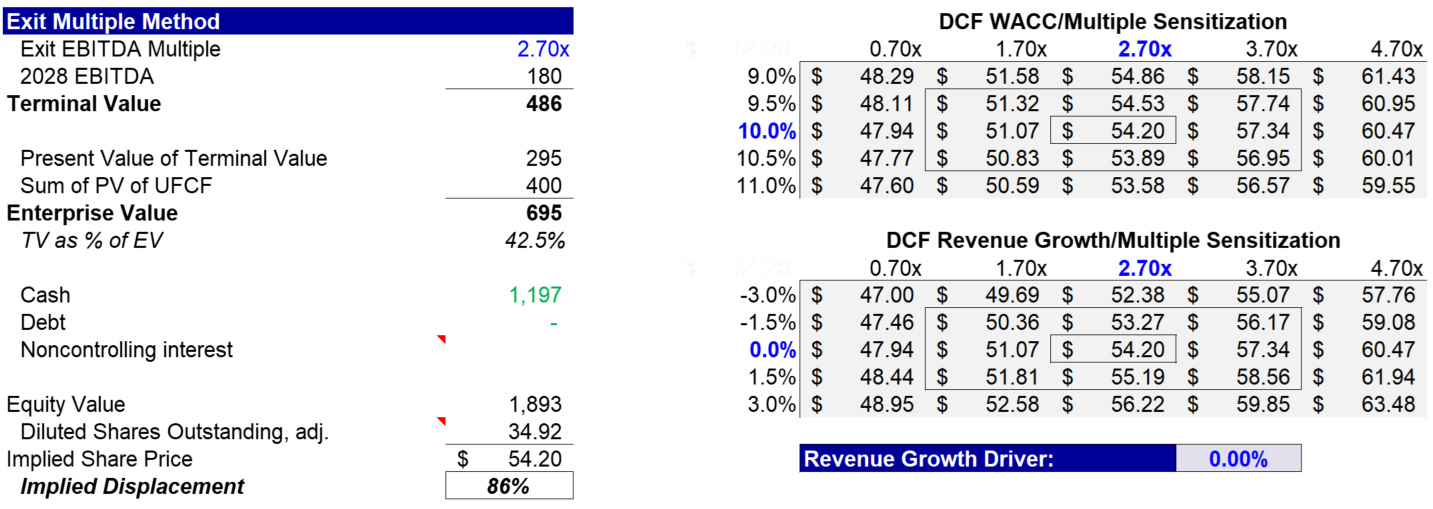

2.7x EV/EBITDA. This is the current multiple, but Taro’s 5 year trading average is 8.33x.

Despite major one-time costs cited by management in COGS and SG&A that should vanish over the next few years, I think the uncertainty here justifies a first-look at a bear-case model and assumptions.

On a DCF Basis (BEAR CASE):

An implied price per share of $54, which is a 86% upside from current levels.

On a DCF Basis (BASE CASE):

Using a reasonable multiple of 6x, still two turns below Taro’s 5-year trading average of 8.33x, I get an implied price per share of $64, 122% upside from current levels without adjusting my conservative revenue and margin assumptions.

The above valuation methods don’t account for any acquisition premium on top of the fair value of the business. Returns are biased to the upside in this situation.

2028 Forward Analysis (BASE CASE):

In my opinion, the truest valuation method is if we can achieve a double over 5 years of investment. The DCF method computes only displacement - the double method computes expected return.

Accounting for interim levered free cash flows, the value of this investment at the end of 2027, on a 2028 forward EV/EBITDA multiple, is $81, representing 177% upside from present.

Realistically though, how much does valuation matter here? You can assume a terrible business outlook and a multiple that’s just plain unrealistic, and the business still generate solid upside - because on the products Taro does sell, it generates solid free cash flow. The business is a bank and balance sheet booster for Sun Pharmaceuticals.

Comps

Using named peers, the table below shows Taro trading at significant discounts to peers. Please note the size differences; difficult to find clear generics comps for Taro.

Investment Horizon, Trade Feasibility, Mechanics

As Taro is under Israeli corporate law, I’ve derived positions sizes and strategies in the context that an investor will operate in. Israel’s stock market is characterized by highly concentrated ownership, with typically one controlling shareholder or group. This has led to a well-developed framework for minority shareholder rights, which provides significant recourse and protection for minority investors. OECD estimates in 2012 indicated that the overall average free float in Israel was 31%, and I haven’t found anything to indicate significant change from that number.

Position sizing on this trade is highly variable. The max position size is 15% of common stock, approximately $165mm – Taro’s articles prohibit a position above 9.9% voting power to avoid classification in the US as a Controlled Foreign Corporation. The minimum position size to be impactful is 3% of common stock, $33mm. Any less and your votes against a merger would independently be insufficient to force a majority-of-minority vote (proxy battle).

The recommended sizing is a 7.5% common stock stake (5% of voting), as at that point the investor has enough control to block a tender offer and negotiate on equal footing with Sun.

A better alternative than a large stake is an activist firm entering the picture and initiating a proxy war. At 1.5% of common stock, the activist can nominate directors for the board and push for change. Currently, there are three independent/external directors on the board of eight. With Israel’s stringent minority shareholder protections, Sun Pharma and the activist would be courting the same set of Taro investors, the largest of which are shown below.

Float and low volume are major issues with this trade – approximately 21k shares are traded on average daily, a value of $630k. Entering a position would likely push the market upwards. Block trades directly with the larger holders above can mitigate this risk and provide for a quick position entry.

The time horizon and catalysts depend on the activist investor. At current rates of buybacks, Sun must initiate its a tender offer in mid-2028, but a fund building a sizable position could potentially be met with pushback from Sun. Sun wouldn’t want to pay elevated prices on a tender offer, and would ideally propose an early buyout offer, before the new investor builds proxy relationships or a sizable stake.

Risks to Thesis

Dramatic deterioration in the generics or dermatologic drugs market, specifically in terms of price deflation, can have a significant negative impact on the potential of Taro’s core business. However, it’s two-part thesis – Taro still has the margin flexibility to cover cash operating cost, which sets the lower bound of trading at the liquidation value of equity.

Litigation risk has been significant for Taro over the past three years. In 2021, Taro made a large provision for losses, which still has significant capital remaining after the recent settlements and resulting EBITDA adjustments. I doubt the materiality of litigation in changing a decision to invest – part of the litigation risk is simply class action suits, a product of the industry Taro operates in.

Value destructive investments from Taro are another major risk, though one that I view as unlikely due to the importance of Taro to Sun. If Taro’s CEO significantly changes gears and actually begins pursuing business development opportunities, Taro could deplete its liquid assets without generating equivalent value from resulting growth.

The last, and potentially biggest, risk is Sun refusing to ‘play ball’ with the investor. If Sun obstructs the activist investor, refusing to communicate or to make operational changes, the activist still has clear recourse. As mentioned earlier, Israel has strong protections for minority investors, and as long as the activist succeeds in working with other minority investors, the minority investors should be able to capture two board seats. Sections 191, 192, and 193 of Israel Company Law define the controlling shareholder’s duty of fairness through the unfair prejudice doctrine. This doctrine is both a final recourse and a key asset in a negotiation.

As cited in a European Corporate Governance Institute Law Working Paper,

“C.A. 5025 Prat Ta’asiyot Matechet Ltd. v. Dadon (28.2.2016). Israeli courts have reinforced minority shareholders’ reasonable expectations by forcing the declaration of dividends or even drafting provisions into the company’s foundational documents to ensure future collaboration. Although court ordered company liquidation is rare, recent cases have resulted in mandated buy-outs to resolve irreconcilable acrimonious shareholder relationships.”

Israeli courts have a history enforcing minority shareholder reasonable expectations in cases of unfair prejudice through control, and an activist investor can be assured of solid ground to stand on when urging Sun Pharmaceuticals to engage in value-additive activities rather than stagnation.

Conclusion

Taro is a uniquely special situation – a business that is a textbook setup for a buyout.

Sun, the strategic, has clear interest in purchasing Taro. Sun has a strong acquisitive history.

Taro, less than a year ago, was buying back shares at prices above $70. Right now, Taro is trading below cash, and the core generics/Alchemee business is effectively free.

Taro is a very important part of Sun’s business, representing 25% of net assets.

Taro has a free cash flow yield of ~12%.

If Sun is given the option, I believe Taro will be taken out well below cash in the next five years. Sun owner Dilip Shanghvi has found a cash cow that he’s played to perfection – driving down volume and float, decreasing management engagement, and avoiding making waves, all to set up a buyout in the next few years. A motivated investor can secure a fair price on the business for themselves and other minority shareholders, earnings a massive premium on current levels.

Disclaimer

This research report expresses my research opinions, which we have based upon certain facts, all of which are based upon publicly available information, and all of which are set out in this research report. Any investment involves substantial risks, including complete loss of capital. Any forecasts or estimates are for illustrative purpose only and should not be taken as limitations of the maximum possible loss or gain. Any information contained in this report may include forward looking statements, expectations, and projections. You should assume these types of statements, expectations, and projections may turn out to be incorrect.

I assume no responsibility or liability for any errors or omissions in the content of this report. The information, opinions and views contained herein have not been tailored to the investment objectives of any one individual, are current only as of the date hereof and may be subject to change at any time without prior notice.

The information contained herein is not, and shall not constitute an offer to sell, a solicitation of an offer to buy or an offer to purchase any securities, nor should it be deemed to be an offer, or a solicitation of an offer, to purchase or sell any investment product or service.

How do you do it? Where do you find this stuff